Consumer payments studies are one of the most widely used – albeit imperfect – ways of understanding changes in consumer payment behaviour. In the last month or so three such studies have been released looking at payments in notably different economies: Switzerland, Jamaica and Australia. Given the proximity of their release it provides an opportunity not just to understand what is happening in each country, but to look at them comparatively. The big lesson that we see is this: consumer perceptions of cash follow a predictable and remarkably stable pathway.

About the studies:

The Swiss National Bank conducts an annual study of consumer payment methods – you can find them here: https://tinyurl.com/snbpmtsurvey. The current study was conducted in the Swiss autumn of 2025 and surveyed around 2,000 individuals.

In Jamaica, BRANCCH Consulting & Outsourcing commissioned the Payment Preferences in Jamaica report. The report sampled 615 people in mid-2025 and asked respondents to complete an extensive survey exploring payment methods and preferences.

The Reserve Bank of Australia has conducted a triennial consumer payments survey since 2007, with the most recent study conducted in 2025, through a wallet diary and survey of around 1,200 consumers.

Three countries with very different characteristics

Switzerland is a country that maintains high levels of cash usage while also having one of the strongest (and most highly trusted) banking systems in the world, along with strong technology adoption generally and payment technology availability specifically.

Jamaica is a developing economy with a rapidly developing payment ecosystem, but also a large informal economy. This means that the banking system, in particular traditional/formal banking services including payment rails, have not gained as much traction as in some economies. Notably, Jamaica is one of only three countries that have launched a retail CBDC (“JAM-DEX”) for general use.

Australia is recognised as a country with early and widespread adoption of digital payment technology, from early adoption of ATMs through to one of the first domestic payment schemes (eftpos) and rapid uptake of contactless and then mobile payments.

What do the studies say and how do they compare?

Here’s a run-down of what the studies each say…

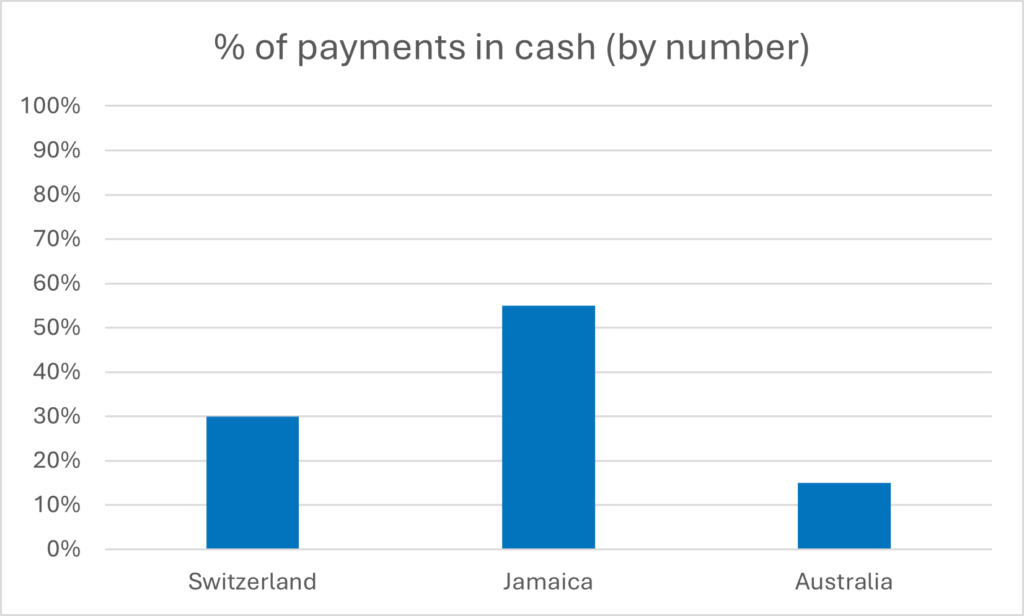

Switzerland has 30% of payments in cash, which is fractionally lower than in 2024. Looking at history we can see a substantial drop as a result of COVID (cash was used for over 70% of payments in 2017), however there appears to be a stabilisation at the 30% level. This is despite effective saturation of digital payment methods – between 80% and 99% of respondents have a debit card, mobile payment apps, and access to online banking (and 78% have a credit card). 70% want the option of using cash not to change, and a further 25% believe it is important that cash can be used as required.

In Jamaica, 55% of payments are in cash. Having cash as an option for payment is either important or very important for 71% of people. One detractor from digital payment adoption appears to be technical reliability of digital payments and POS devices – higher than in other countries. Given Jamaica’s launch of a retail CBDC, it is interesting to observe that 89% of respondents did not use the digital currency.

Australia had an increase in cash usage from 2022 to 2025, with 15% of payments by number and 19% of in-person payment by number made in cash (2022: 13% and 16%, respectively). The 15 years prior showed a consistent decline – with cash payments accounting for 70% of transactions in 2007 – pointing to a bottoming out of this trend. The RBA points to other higher-frequency indicators (eg. ATM withdrawals) that support this observation. Interestingly, half of respondents used cash in a typical week, and around one-third said they would face hardship or major inconvenience if cash became difficult to access (including 24% of respondents who were “no” or “low” cash users).

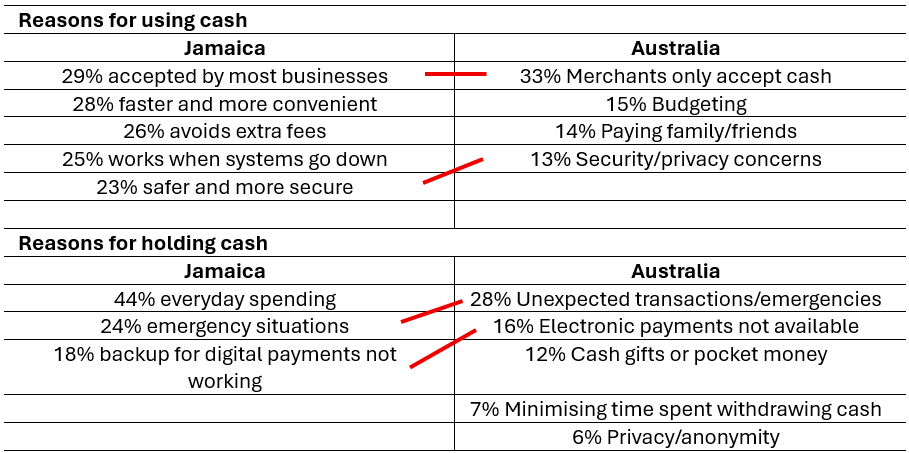

Both Jamaica and Australia published survey responses for why cash is used and why it is held. Despite the significantly different levels of cash use in each country and the different context, there are certainly similarities:

Making sense of the surveys

What we can see from this data is three economies and payment ecosystems in very different stages, but with a number of rhyming messages.

- Flattening usage is more likely than continued decline. Both Switzerland and Australia demonstrate a flattening trend – Switzerland at around 30%, Australia at around 15%. We acknowledge that both of these are only two surveys of flattening, but this aligns with other data points (as the RBA indicated). The level of usage where the trend flattens evidently differs by country, but the message suggests that system planning, infrastructure and policy should anticipate this phenomenon

- Consumer reasons for cash usage appear to be similar. While there are differences depending on the stage of evolution of payment behaviour, consistent themes such as merchant payment acceptance, security and privacy, cash as a back up and the reliability of digital payments are found whether the country is a high or low cash environment

- Consumers have a strong stand on the ongoing role of cash. In various ways, all three surveys pointed to a societal expectation that cash must continue to be available and readily accepted

- Demographics are a consideration, but shouldn’t be deterministic. While all surveys suggested higher cash usage in older populations, we see combinations of widespread usage in younger populations, and/or an expectation of inconvenience or hardship if cash were to not be available or expected even amongst low cash users. Policymakers should be careful in assuming too much from demographic trends

- Cash infrastructure is worsening and is critical. Specifically consumer cash access infrastructure – ATMs, branches, etc – is pointed to as being an increasing problem. Policy support to maintain the presence of ATMs and branches in order to support cash access is important for supporting consumers. While these studies were consumer-focused, we have observed the importance of branch infrastructure for merchant cash acceptance, which furthers this point

Conclusion

These surveys together point to the long-term need for cash within economies at all stages. However, in all cases the data points to significant change in the cash cycle. Managing change, particularly declining activity paired with a large and costly physical infrastructure, makes for big challenges, whether that be at the consumer, operator, bank, or regulator level. The most important thing to be doing is to be aware not just of high level markers such as cash usage, ATM withdrawals or currency in circulation, but to get under the hood and understand where the pressure points are already presenting within the cash system.

Sources: BRANCCH Consulting and Outsourcing Limited, Payment Preferences in Jamaica Report (2026); Swiss National Bank, Results of the Payment Methods Survey of Private Individuals 2025 (March 2026); Reserve Bank of Australia, Cash Use in Australia: What the 2025 Consumer Payments Survey Tells Us, RBA Bulletin (April 2026).